For ease of reading, we have broken out the pension plan information into sections listed on the left. Simply click on each title to display that section. Participants in the CGF Pension Plan, please contact our office for personal information. Click Here.

PENSION PLAN GENERAL INFORMATION: OVERVIEW

The Pension Plan for Agricultural Employees of Member Employers of the California Grower Foundation (the “Plan”), was established in 1973 to meet the following objectives:

- portable benefits to non-permanent workers

- a convenient source of supplemental retirement income

- a valuable benefit for long term employees

The Plan is a qualified Multiple Employer defined benefit plan . All participating Member Employers contribute to the Plan at the same rate, combining assets to pay retirement benefits to their employees.

The Pension Plan Committee, which is composed of CGF Board members, is responsible for oversight of the Plan. The Committee meets with advisors (pdf) on a regular basis to monitor Plan stability. The cost of the Plan is based on economic and financial assumptions. Contribution and benefit levels have evolved over time to meet the needs of Member Employers and their employees and to comply with ever-changing regulatory requirements.

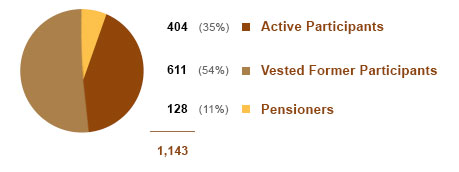

Since inception, the Plan has provided pension benefits to over 2,100 participants and paid over $20.5m in pension benefits.

Participating Employers: Member Employers

California Grower Foundation

Frediani Vineyards

Gallo Vineyards*

Hoot Owl Creek

Hanna Vineyards

Steltzner Vineyards

Swanson Vineyards

Treasury Wine Estates

Treasury Chateau Wines effective 1/1/16, formerly Diageo Chateau & Estates Wines

York Creek Vineyards

*Gallo provides the CGF Pension Plan under an agreement with the United Farm Workers

As of January 1, 2015

Additionally, the Plan has identified 175 “missing participants” — employees whom we have been unable to locate or contact. The Plan routinely attempts to search for missing participants internally. Periodically, the Plan uses the Pension Benefit Information address location service. Un-locatable participants are not included in calculating Plan funding targets, although they are included in determining Plan liabilities should the Plan be terminated. Fees must be paid to Pension Benefit Guaranty Corporation (PBGC) on behalf of missing participants.

Financial Information: General Overview

The financial status of the Plan is continually monitored internally by the Pension Plan Committee and Plan advisors. It also is monitored through regulatory agencies.

The Plan’s annual report is filed with the U.S. Department of Labor, and as required by ERISA, is sent to all Plan participants and Member Employers. To view the most recent Funding Notice, Click Here (pdf).

Plan financials are audited annually and also serve as the basis for the required annual report (Form 5500 Click Here ), filed by CGF on behalf of all participating Member Employers. In 2014, Plan administrative expenses were 1.80% of total assets and include Actuary services, Pension Benefit Guaranty Corporation fees, Trustee/Custodian and UB banking fees, accounting and auditing, legal counsel, investment advisor, fiduciary liability insurance and other miscellaneous items such as printing costs, filing fees, etc.

All contributions are held in trust by US Bank.

For a complete copy of any of the financial reports noted above, or Actuarial Valuation, contact Becky Barlow bbarlow@calgrower.org.

Financial Investments

The primary objective of the Plan investment policy is to achieve consistent, long term returns which meet or exceed prevailing market conditions. The portfolio is well diversified and relatively conservative.

Assets are allocated among the following classifications with at least two managers in each class:

| US Equity | 34% |

| Fixed Income | 48% |

| International Equity | 15% |

| Cash | 3% |

| Total | 100% |

The investment advisor provides quarterly Performance Measurements reports, monitors asset allocation and makes recommendations as needed to achieve Plan objectives.

Funding Requirements

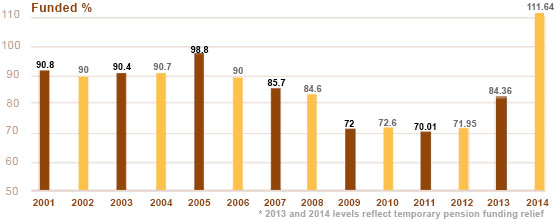

In simple terms, the funding percentage is determined by Plan assets divided by the current liability (the present value of future benefits owed to all Plan participants). Until recently, target funding levels of 80%-100% were deemed sufficient.

The graphic below illustrates Plan funding levels since 2000:

The Pension Protection Act of 2006 (PPA) completely overhauled minimum funding rules that have been in place since ERISA was signed in 1974. PPA required pension plans to reach fully funded status by the year 2015. However, market conditions have made that target difficult to attain. First, pension plans incurred large investment losses in 2008. Secondly, interest rates have declined since 2008, thereby raising pension plan liabilities. In response to the financial strain than plan sponsors faced in order to comply with the full funding target set by PPA, Congress passed several rounds of legislation which gave plan sponsors funding relief that effectively pushed the full funding target date beyond 2015.

For a more detailed description of PPA legislation see: http://www.dol.gov/EBSA/pensionreform.html

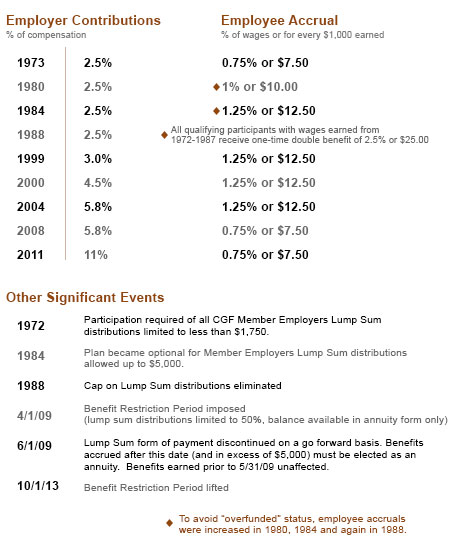

Although the Plan meets current funding requirements, actuarial projections confirmed that changes to the Plan would be necessary to attain the objective of 100% funding by 2015. Effective July 2008, future benefit accrual levels were reduced from 1.25% to .75%.

As a result of the funding level, the plan entered into a Restriction Period beginning April 1, 2009 limiting the distribution of lump sum payouts. If vested benefits are more than $5,000, participants may elect (a) 50% lump sum/50% annuity (b) 100% annuity or (c) defer payout until the restriction is lifted. After June 1, 2009, lumps sum will no longer be available (unless totaling less than $5,000). See Benefit Descriptions page for details.

Liabilities and Obligations

In the CGF multiple employer defined benefit plan, all participating Member Employers contribute to Plan assets and share a financial obligation to fund their allocated share of the Plan’s unfunded vested benefits.

In the event a Member Employer chooses to withdraw from the Plan, the Member Employer’s withdrawal liability will be determined using the most recent date the Plan’s assets and liabilities were valued and allocated based on that Member Employer’s percentage of total contributions made during the most recent five years.

The withdrawal liability for a Substantial Employer is the greater of the liability calculated by the Plan actuary or such amount as determined by the Pension Benefit Guaranty Corporation (PBGC)

As outlined in the Procedures for Withdrawal, upon receipt of timely notification to CGF, the liability amount will be determined after verification of wages and contributions. It is the responsibility of the Member Employer to notify its employee-participants of Plan withdrawal. Participants are not entitled to distribution of benefits until they retire or terminate employment.

In the event all Member Employers decide to terminate the Plan (Mass Withdrawal). it will be considered a Standard Termination only upon showing PBGC that the Plan has enough money to pay all benefits owed to participants. If funds are insufficient, Member Employers would have to fund withdrawal liability plus expenses or initiate a Plan Freeze by closing the Plan to new entrants and/or ceasing accruals for Plan participants to allow assets to reach sufficient funding to terminate the Plan under a Standard Termination.

If the Plan does not have enough money to pay benefits owed and if participating Member Employers are financially unable to fully fund the Plan, a Distress Termination may occur. In that case, the PBGC would assume the Plan’s obligations and seek collection from current Member Employers and any former Member Employers who have withdrawn within the previous 5 years.

Benefit Descriptions

An explanation of Plan participant benefits is contained in a simple, easy to read format in the Summary Plan Description (pdf) booklet.

The technical source of Plan language is the Plan Document (pdf), restated effective January 1, 2012. The Plan Document incorporates all statutes, regulations and other guidance as required by the IRS. On occasion, the Plan is amended to reflect revised language or regulations. To meet IRS notification requirements, CGF will mail amendment notices directly to Plan participants with a copy to the Member Employer.

Each year, the Plan will provide active participants with a Benefit Statement (pdf), showing an estimate of monthly* pension accumulated, based on years of service and wages earned, and projected earnings at retirement age of 65. Benefit Statements are typically generated within 6 months following the close of the prior calendar year and mailed to the Member Employer for distribution to its employee-participants. Statements for non-active participants are available upon request.

* Benefit Statements do not reflect lump sum estimates due to actuarial factors which vary from year to year.

Benefit Eligibility

The criteria for Plan participation was established by the Member Employer in the CGF Member Agreement and is typically limited to all agricultural employees. In some instances, the Member Employer also may have extended eligibility to other job classifications (winery employees, administrative staff, managers, etc.).

Sole proprietors, partners, independent contractors and leased employees are not considered eligible employees. Highly compensated employees as defined by the Internal Revenue Code also may be deemed ineligible.

Contributions must be made to the Plan on behalf of all eligible employees for all taxable W-2 wages including base pay, overtime, severance and/or bonus earnings. Periodically, CGF will request payroll records to confirm accuracy of eligibility reporting and to resolve any discrepancies. Eligibility data is verified by the Plan actuary and through the annual accounting audit.

An Employee hired after 8/1/04 becomes a participant six months after the later of the dates below:

- The first day of the month after total earnings exceed $4,000; or

- The first day of the 13th month after the employee is hired and any earnings have been made on his/her behalf

If hired prior to 8/1/04, an employee became a participant as of the first day of the month:

- After completion of one Year of Service in a Plan year; or

- Following one full year of employment and completion of one Year of Service during that one year period

Participation ends when the employee terminates employment with a Member Employer, retires at Normal Retirement Age of 65, elects Early Retirement, in the event of Total Disability or at time of death.

Eligible beneficiaries may include a spouse, child or children (including adopted children) of married participants.

Vesting

Vesting is the employee’s right to receive benefits accrued under the Plan on his/her behalf. An employee begins to earn vesting credit when he or she becomes a participant. Full vesting occurs:

- upon completion of at least 5 Years of Service with any Member Employer without having an intervening Break in Service

- after attaining age 65 and if still working for any Member Employer

Effective August, 1, 2004, a Year of Service is a calendar Plan Year in which earnings exceed $4,000. The employee will be credited with only one Year of Service during any Plan year. A Break in Service is five consecutive years in which earnings are less than $4,000.

Prior to August 1, 2004, a Year of Service was calculated on the basis of credit; ¼ Year of Service for every $25 contributed by the Member Employer in a Plan Year, up to a maximum of 2 ½ Years of Service during any Plan year. A Break in Service was any Plan year with less than 500 hours of service or in which less than $25.00 was contributed by a Member Employer.

If a Member Employer withdraws from the Plan, service for that Member Employer will not count as a Year of Service after that withdrawal.

Accrued benefits are forfeited if employment is terminated prior to completion of 5 Years of Service or Normal Retirement Age.

Benefit Distribution

The Plan was initially designed to provide a monthly annuity at retirement. Lump sum distributions were available only for retirement benefits of less than $1,750. This feature eventually was eliminated to provide a greater sense of value and financial security and to accommodate employees who were concerned about the safe delivery of their monthly pension checks in Mexico.

The monthly annuity amount and duration depends on whether the participant

is single or married:

- Single employees receive a single life annuity payable over their lifetime.

- Married employees have the option to receive a single life annuity or joint and survivor annuity. The joint and survivor annuity provides a monthly lifetime pension to the employee and upon his or her death, the spouse receives a monthly benefit for the remainder of that spouse’s life. Notarized spousal consent is required to waive the joint and survivor annuity in lieu of a life annuity or lump sum benefit.

Eligible participants electing distribution during this period will be unable to receive full lump sum payout. They may elect 50% lump sum/ 50% annuity, a full annuity distribution or may defer payment until the Benefit Restriction Period ends.

In an effort to reduce nominal lump sum distributions, the Plan was amended to increase the minimum lump sum distribution to $5,000.

Additionally, after 6/1/09 all benefits earned in excess of $5,000 will be paid in the form of annuity only. Benefits earned prior to 5/31/09 are not affected (unless paid during the Benefit Restriction Period as explained above).

Whether single or married, the employee may waive the annuity form of benefit only before benefits begin. Once the pension benefit starts, it cannot be changed.

The lump sum is the cash equivalent of the monthly annuity and is calculated using a formula based on earnings, age and interest rate. The interest rate factor is provided annually by the government. Because the interest rate factor varies from year to year, the Plan does not include lump sum amounts on the Annual Benefit Statement. This information is provided to terminated employees or those anticipating retirement within the Plan year.

CGF does not provide investment or tax advice and always suggests the employee make decisions only after careful consideration and consultation with experienced tax and financial advisors.

How Benefits Are Calculated: Benefit Accural

Benefits are based on all of the following:

- the employee’s years of service

- eligible earnings contributed to the Plan on the employee’s behalf (rounded to the next lower $1,000)

- benefits accrued during the Plan year

For every $1,000 of wages paid, benefits accrue during the Plan Year at the following levels:

| 1972-1979 | $7.50 |

| 1980-1983 | $10.00 |

| 1984-6/30/08 | $12.50 |

| 7/1/08 | $7.50 |

Note: All qualifying participants with wages earned from 1972-1987 receive a one time double benefit of $25.00

Calculation Example:

Juan Ruiz, hired at Doe Vineyards in 1982 and retired in 2007:

1972-1987 earnings total $197,000 x $25.00=$4,925

1988-2007 earnings total $862,000 x $25.00=$10,775

ESTIMATED BENEFIT:

Annual benefit $15,7000

Monthly benefit $1,308

Lump sum benefit

at age 65 (using 2008 age factor for 65 = 12.120776) $190,296

at age 58 (using 2008 age factor for 58 = 8.266000) $129,776

Amounts shown do not reflect mandatory federal withholdings, optional state withholdings or if applicable, early distribution tax.

Early Retirement benefit is the total of each year’s credit until date of early retirement reduced by ½% for each month payments begin before age 65.

Disability Retirement benefit is the total of each year’s credit until date of disability reduced by ½% for each month payments begin before age 65.

Tax Implications

Federal income taxes will be withheld automatically from lump sum distributions, unless the employee authorizes a transfer to another qualified plan or IRA; Federal income taxes on annuity payments and state income taxes on any form of distribution will be withheld unless the employee elects otherwise, in writing.

| US Equity | 20% |

| California (optional) | 10% of Federal withholding |

| Early Distribution Tax | 10% (applicable if prior to age 59½) |

Employees electing not to have taxes withheld are responsible for payment of taxes and/or any penalties that may apply.

Taxation of payments may vary by residency of the recipient, as the Tax Treaty between the U.S. and each country vary. Article 19 of the Tax Treaty between the US and Mexico provides that residents of Mexico (non-U.S. citizens or permanent residents) will be taxed by Mexico.

Claim Process

The claim process begins when the employee notifies the Plan of retirement or termination of employment. Processing time is typically 90—180 days, provided all necessary information is received on a timely basis from the employee.

Provided all information is completed on a timely basis, the Normal Retirement Benefit will begin on the first day of the month after the employee stops working.

Early retirees should notify the Plan 90 days in advance of intent to retire at age 55 (or after 5 Years of Service).

Disability Retirement Benefits may be requested at anytime after the determination of total disability.

A vested participant who terminates employment with a Member Employer and who is under age 65, may elect early distribution; however, a full year with no contributions made on that employee’s behalf must occur to receive a lump sum payment.

Plan benefits may be directed to pay certain obligations resulting from court ordered child support or alimony under a Qualified Domestic Relations Order (QDRO). Such an order can force payment of benefits to an alternate payee but not before the participant is eligible to receive payment.

If a participant is rehired or hired by a different Member Employer after a lump sum benefit payment has been made, the employee will continue to accrue benefits from the date of rehire. In the event the employee elected a monthly annuity, future payments will be suspended.

In the event of the death of a Plan participant, the surviving spouse is automatically entitled to any death benefit unless the employee (with the spouse’s consent, if married) designated one or more of his/her children to receive death benefits. If there is neither a surviving spouse nor a valid designation of beneficiary, no benefits will be payable.